Macro

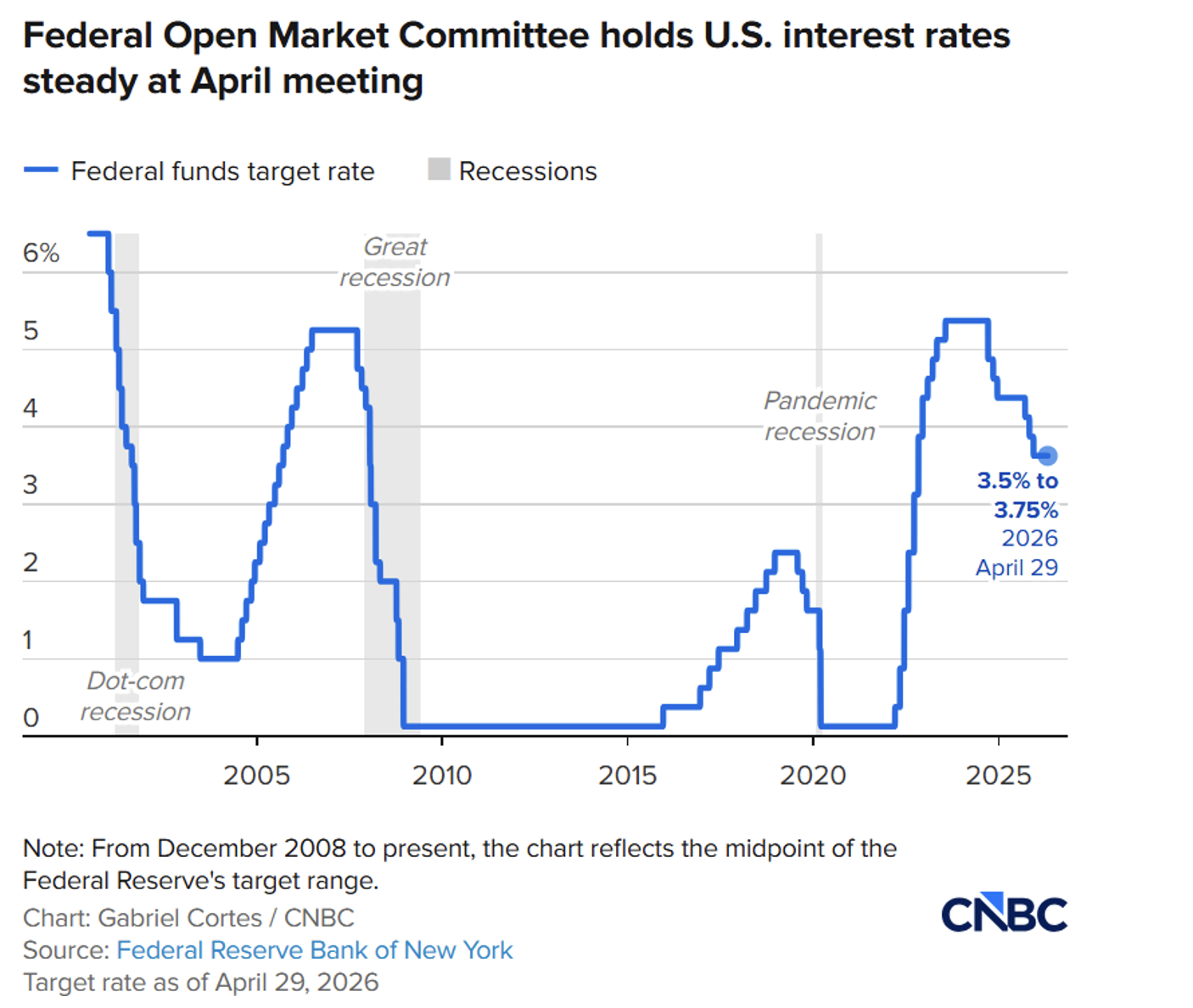

The Federal Reserve’s policy direction remains uncertain, with market participants and economists expressing divergent views on the timing and magnitude of future rate changes. The Federal Reserve held its benchmark policy rate steady at its April meeting, marking the third consecutive meeting where the committee chose to stand flat. The FOMC was split along 8-4 lines, with officials expressing different reasons for their vote; the last time four members dissented was October 1992. [1]

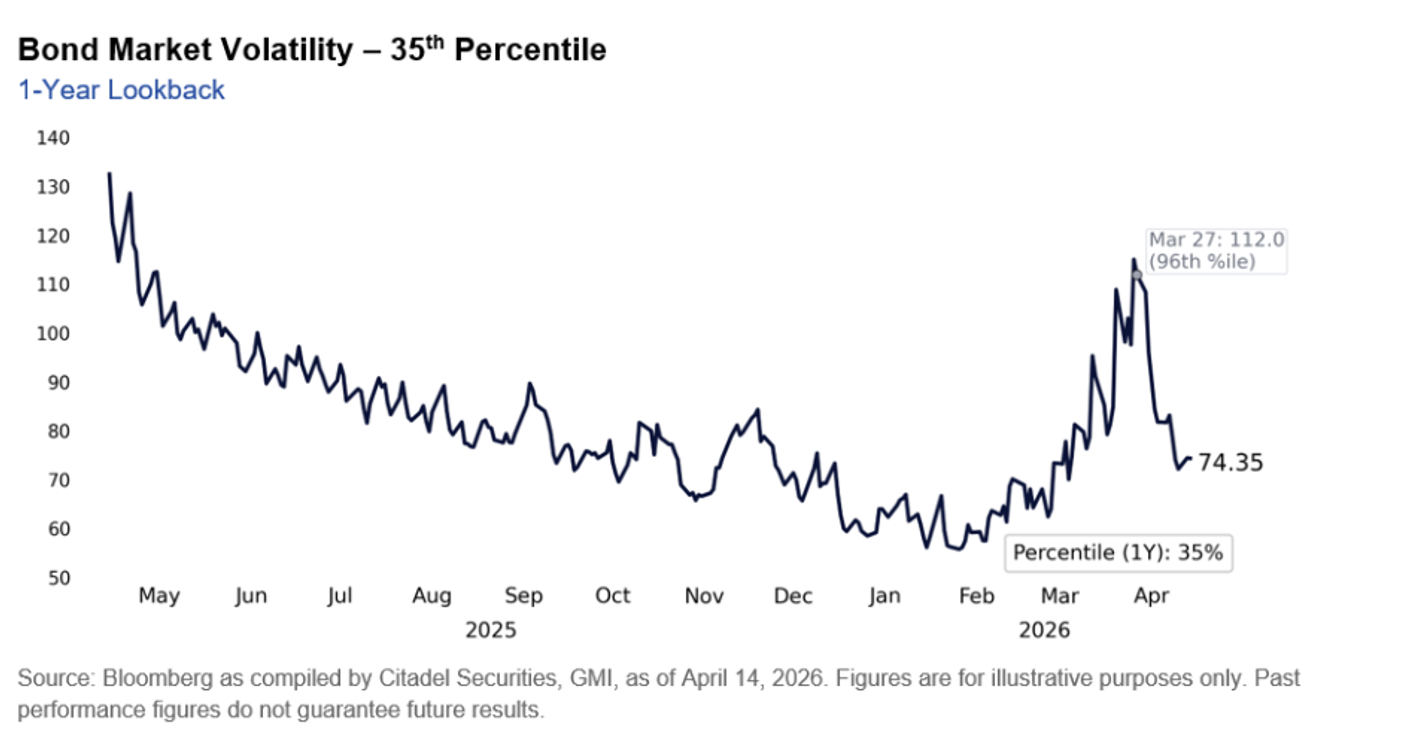

Three of the four dissenters supported holding rates but opposed the inclusion of an easing bias in the statement. [2] Beyond the vote itself, the imminent leadership transition adds another layer of uncertainty. At Kevin Warsh’s confirmation hearing, Warsh called for a “regime change in the conduct of policy” and a new inflation framework, describing the 2021-22 policy errors as a fatal mistake that still weighs on the economy today. [3] Current market expectations around the Fed’s direction should be watched with appropriate caution, the leadership transition, internal divisions, and a still-elevated inflation backdrop make this one of the more uncertain policy outlooks in recent memory. However, it is worth noting that bond market volatility, a useful gauge of uncertainty around the rates outlook, has eased but remains present, with implied volatility in rates markets sitting around the 35th percentile of its one-year range. [4]

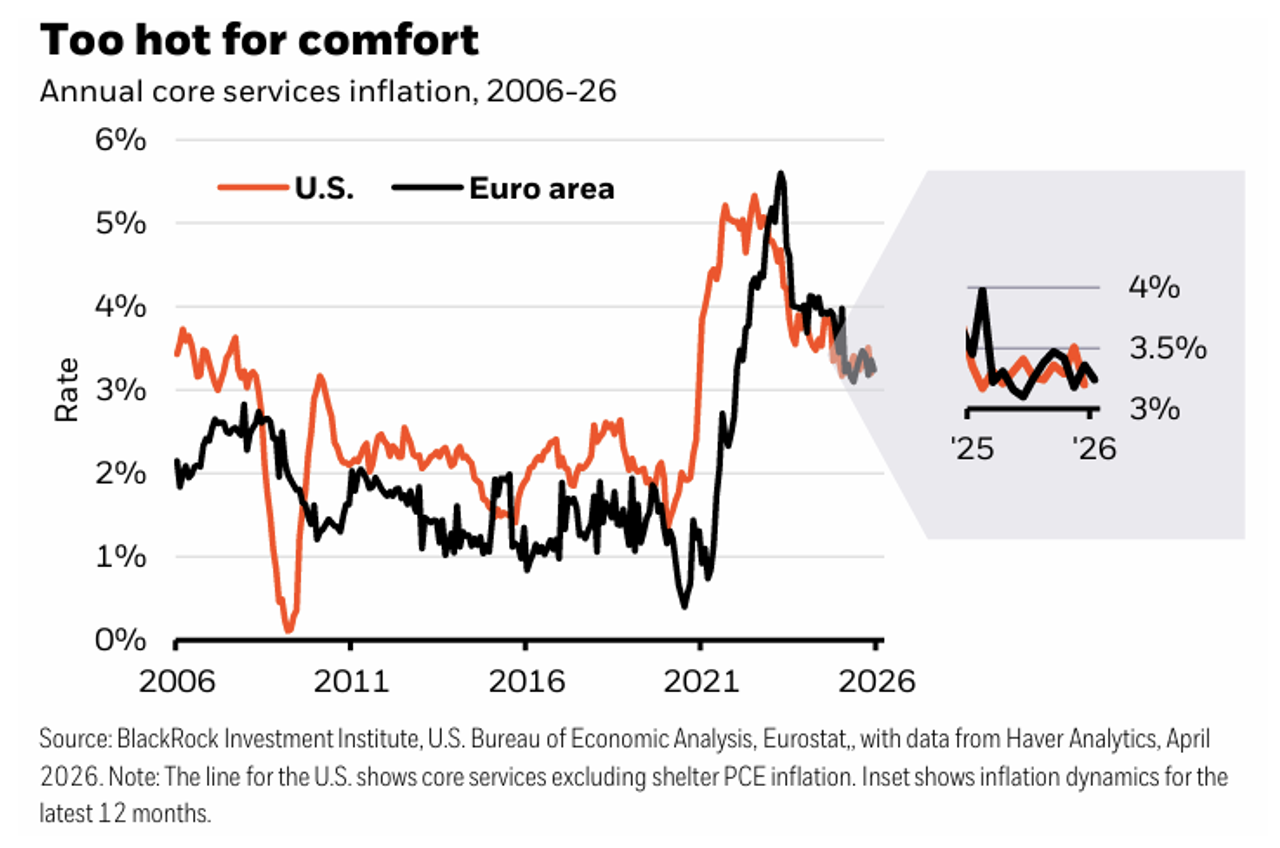

We can expect that inflation remains uncomfortably elevated through mid-2026 before moderating gradually. First, the energy shock has landed on a backdrop that was already sticky. BlackRock notes that core services inflation had already stalled before the conflict began, with structural forces including an aging population, immigration curbs, an AI-driven capital expenditure boom and tariff-driven goods prices all keeping broader inflation above central bank targets. [5]

Second, the commodity disruption extends well beyond oil. The Arabian Gulf accounts for at least 20% of all seaborne fertiliser exports and around 46% of global urea trade, [6] meaning that supply disruptions are feeding directly into food and agricultural input costs. These second-round effects on food and manufacturing costs are likely to keep inflation pressures broad-based, even if headline energy pressures ease.

Third, while a resolution is likely, it will not be swift. The incentive structure for both the US and China points toward resolution, but a gradual one. On the US side, President Trump faces a difficult midterm election coming up. On the Chinese side, the pressure is equally real, China’s Gulf oil imports far exceed what it receives from Russia, and standard modelling points to a meaningful GDP hit for every sustained rise in oil prices. [7] Both superpowers are therefore pulling toward a settlement. That gradual easing, set against an already sticky inflation backdrop, is why the Fed might possibly remain on hold well into the second half of the year.

Commodities & FX

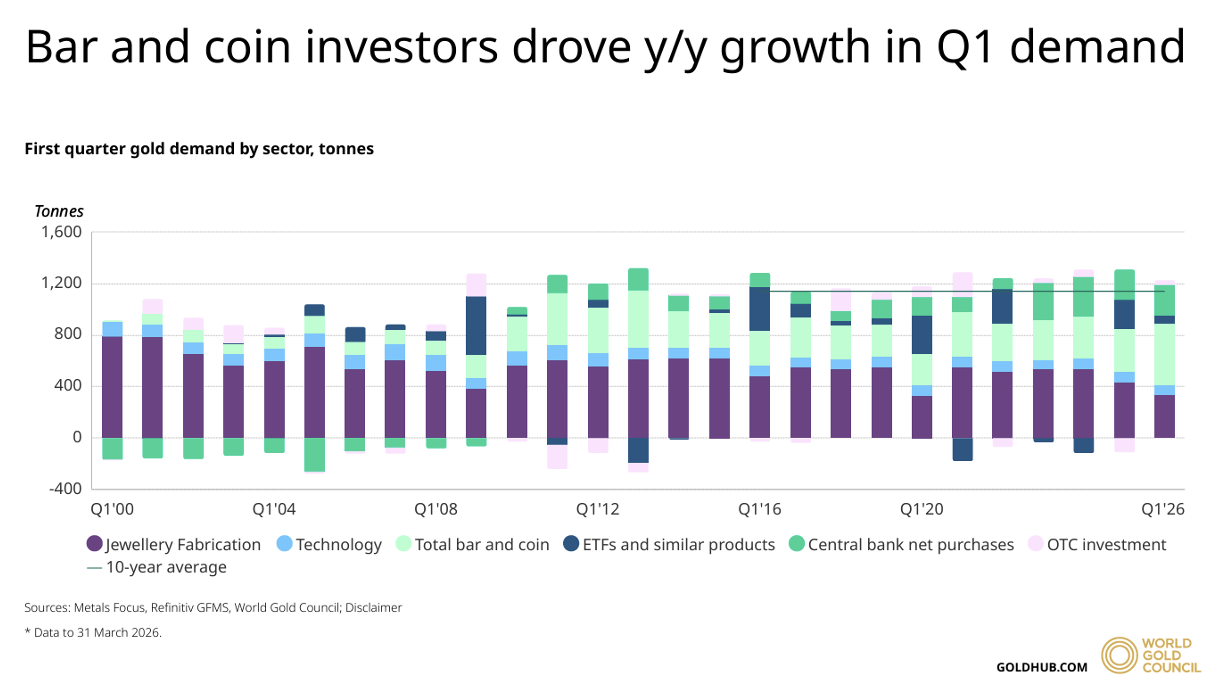

Gold’s structural bull case remains compelling, and the recent pullback from highs looks like a tactical setback within a broader uptrend. The primary engine is central bank demand, Goldman Sachs projects emerging market central banks will collectively purchase approximately 60 tonnes of gold per month throughout 2026, as institutions diversify reserve holdings away from the US dollar and reduce exposure to geopolitical and currency risks. [8] The Iran episode could still possibly accelerate diversification into gold and weighs further on perceptions of Western fiscal sustainability. In an environment of sticky inflation, gold may remain a strategic portfolio allocation.

Brent crude surged to above $120 per barrel on April 29, the highest level since 2022. [9] Prospects for a near-term resolution to the Iran conflict or reopening of the Strait of Hormuz remained dim, with President Trump announcing the US would maintain its naval blockade until Iran agrees to a nuclear deal. [10] Critically, even formal ceasefire progress does not mean immediate supply normalisation, analysts caution that infrastructure damage to Gulf production facilities means supply recovery could take months, limiting the pace of any price decline even in benign scenarios. [11]

Equities

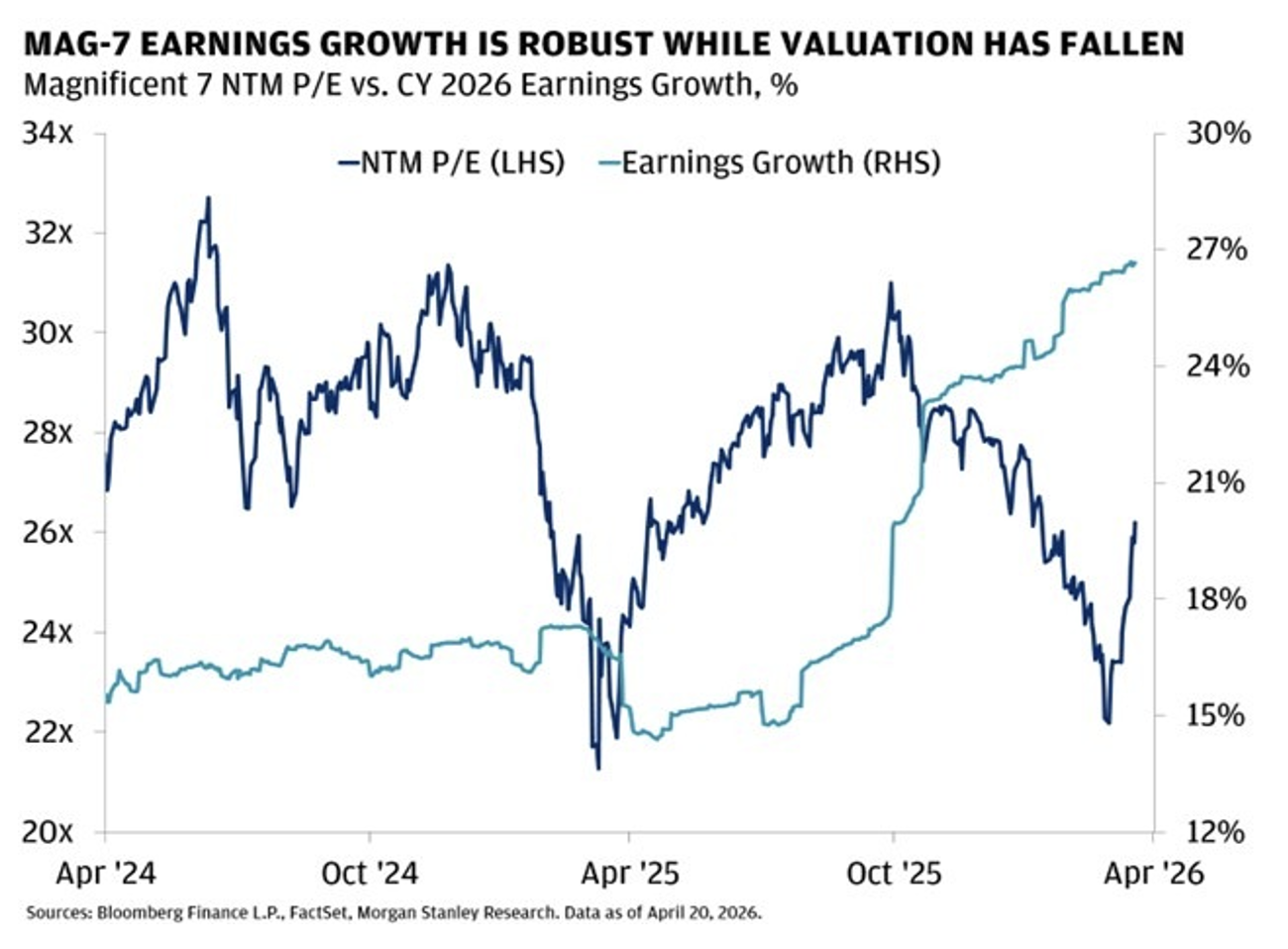

U.S. equities continue to be supported by strong fundamentals, with the Magnificent 7 stocks remaining a key driver of earnings growth. First quarter results from companies such as Amazon, Microsoft, Alphabet, and Meta highlight continued momentum in AI, cloud computing, and digital advertising. Growth remains robust in absolute terms, supported by sustained demand for AI infrastructure and services. [12] In addition, earnings visibility for these companies remains relatively high compared to the broader market, given their scale and more predictable business models.

At the same time, valuations for the Magnificent 7 stocks have come down from previous highs even as earnings expectations remain strong. This suggests that the group is now trading at more reasonable levels relative to its growth outlook. The combination of solid earnings performance and lower valuations provides a more balanced setup compared to earlier periods when valuations were more stretched.

Overall, the US equity outlook reflects continued support from large-cap technology alongside a more complex macro backdrop. While strong earnings and improved valuation levels provide a supportive base, market performance remains influenced by broader factors including interest rate expectations, inflation dynamics, and geopolitical developments. According to UOB Private Bank, regional trends remain mixed outside the US, with more modest growth in Europe and Japan, while emerging Asia shows relatively stronger earnings momentum supported by semiconductor demand and improving trends in key markets. [13]

Fixed Income

Treasury yields have moved higher amid elevated volatility, [14] reflecting persistent inflation concerns and geopolitical developments, particularly in the Middle East. Higher energy prices have contributed to upward pressure on inflation expectations, [15] leading markets to adjust expectations for interest rates to remain elevated.

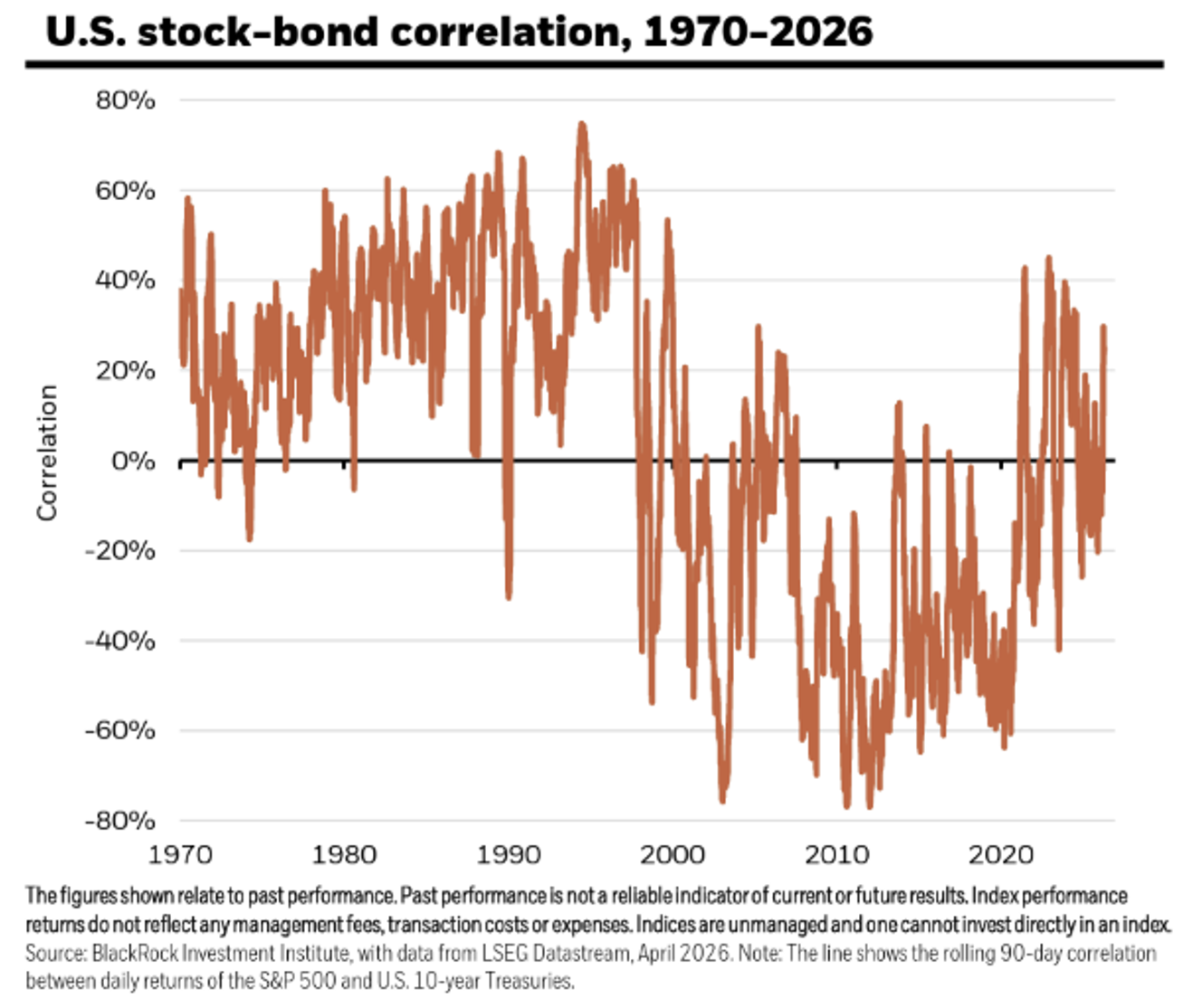

The correlation between equities and bonds appear more positive in recent periods, reducing the diversification benefits of fixed income. Rising yields may have weighed on bond prices while also putting pressure on equity valuations, resulting in both asset classes moving in the same direction at times.

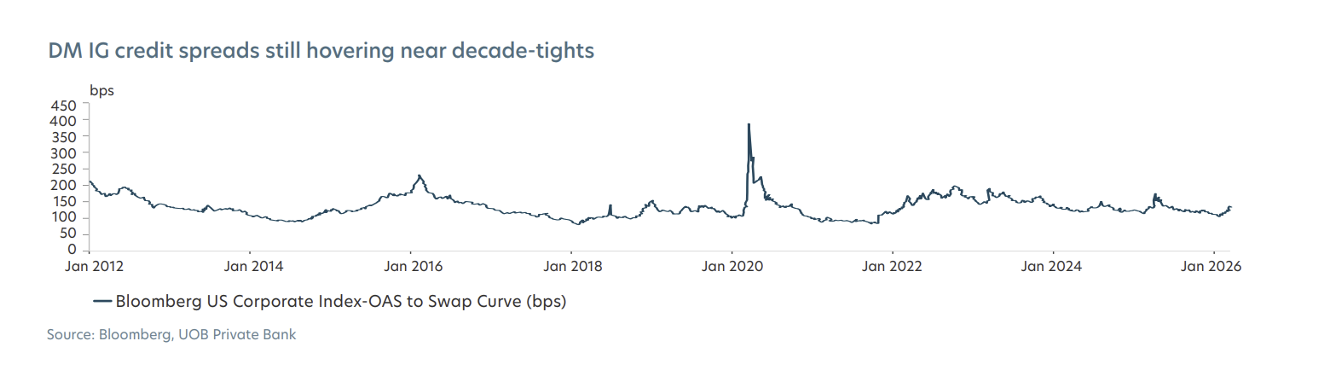

Within credit markets, spreads remain near historically tight levels, indicating limited compensation for taking on additional credit risk. While yields provide some income support, the overall risk-reward profile may appear more balanced given ongoing inflation pressures and geopolitical uncertainty. Fixed income performance may remain sensitive to changes in inflation expectations, interest rates, and broader market conditions.

Source :

[1] Fed interest rate decision April 2026: Fed holds rates steady amid dissent | CNBC

[2] Fed keeps interest rates steady as Iran war fuels inflation | NBC

[3] Kevin Warsh Fed chair confirmation hearing: Live updates | CNBC

[4] Flows and Fundamentals | Citadel Securities

[5] Weekly market commentary | BlackRock Investment Institute

[6] Beyond oil: 9 commodities impacted by the Strait of Hormuz crisis | World Economic Forum

[7] What the war in Iran means for China | Bruegel

[8] Goldman Updates Their Gold Outlook For 2026 | The WealthAdvisor

[9] Oil price briefly hits $120 after reports of ‘extended’ Iran blockade | BBC

[10] Trump Tells Aides to Prepare for Extended Blockade of Iran | WSJ

[11] Why Oil Prices Are Rising? WTI Near $112, Can It Hit $150? New Oil Price Predictions

[12] Tech giants’ results show rosy outlook for AI boom and US stock market | Technology | The Guardian

[13] 2Q 2026 Investment Outlook Resilience amid global complexity

[14] US Treasury yields extend increase, two-year yields at 3.90%, highest since March 30 | MarketScreener

[15] Global inflation worries stir on energy price flare-up, but still relatively subdued – Reuters poll | Reuters