Macro

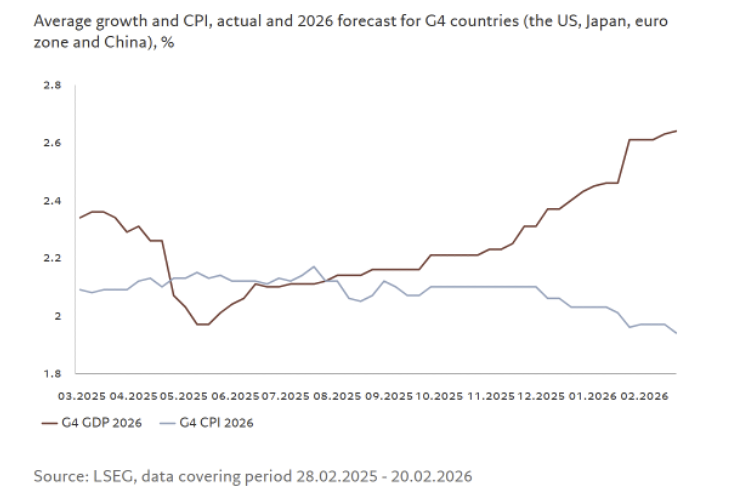

February was a good month for investors with most asset classes delivering positive returns, while economic indicators globally looked positive with strong growth and stable inflation.

The macro backdrop may remain supportive, as most nations are easing monetary policy while also increasing fiscal spend. At the same time, investment in artificial intelligence continues to accelerate. Large technology companies alone are expected to spend more than USD 600 billion this year on building data centres and digital infrastructure. [1]

A key risk area to monitor is a potential slowdown in US household spend as higher energy costs and tariffs pose headwinds. U.S. consumer spend makes up around 70% of the country’s GDP, which makes it a critical pillar of the U.S. economy. Savings rate has fallen to 3.6% (approximately half of normal levels) while Real Personal Consumption Expenditure (PCE) fell to 1.7% (below the six-year average), signalling a moderation in consumption momentum and increasing pressure on household purchasing power.1

Equities

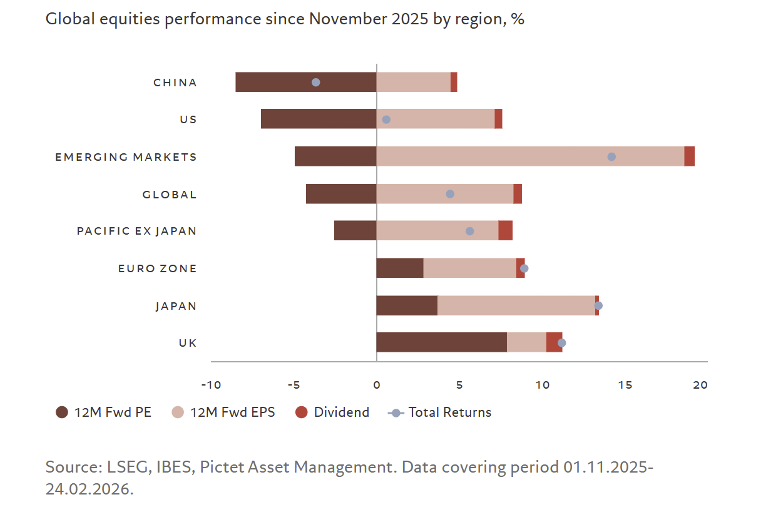

Broadening of global growth continues to play out as small-cap equities and emerging market (EM) equities continue to outperform. By contrast, the S&P 500 was the worst-performing major equity market over the month, delivering total returns of -0.8%. [2]

Indicators suggest global capital continues to flow strongly into equities, which attracted more than USD 100 billion of inflows over the past four weeks. A notable regional divergence has emerged, U.S. share of equity inflows has fallen to its lowest level since 2020, while foreign buying of Japanese equities accelerated following the general election in February. [3]

In the U.S., growth in bank lending and the Federal Reserve’s securities-buying programmes [4] are injecting additional liquidity into the economy, which is already supported by substantial government stimulus and strong AI-related investment. While this liquidity supports asset prices in the near term, the longer it persists, the greater the risk of asset bubbles and renewed inflationary pressures. [4]

Fixed Income

While economic activity remained healthy in February, rising concerns about AI-driven unemployment and geopolitical risks increased demand for safe assets. This supported bond purchases, allowing global fixed income markets to deliver total returns of 1.1% over the month. [5]

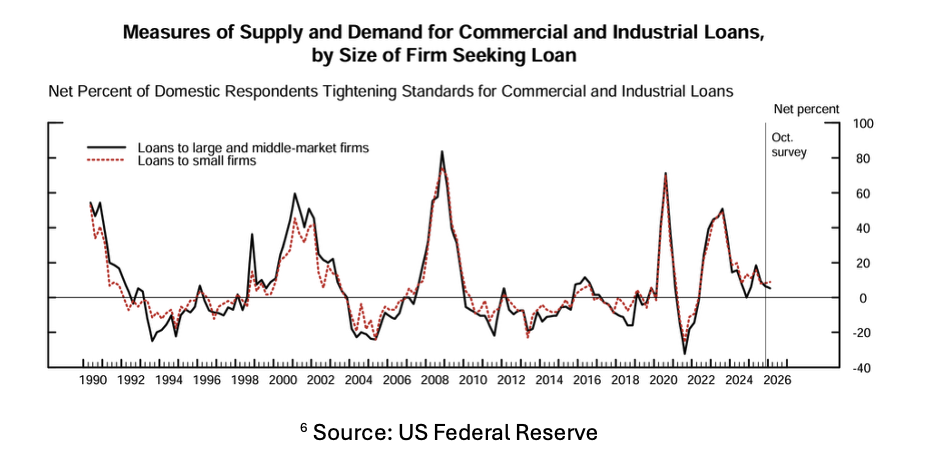

As of March 2026, in our view, the credit cycle looks like it is entering late-cycle but not yet stressed. Public credit still looks fairly healthy: credit spreads have widened recently, but they are still tight versus long-run history; investor demand for corporate bonds has remained strong; and banks say lending standards are mostly unchanged rather than tightening sharply. [6]

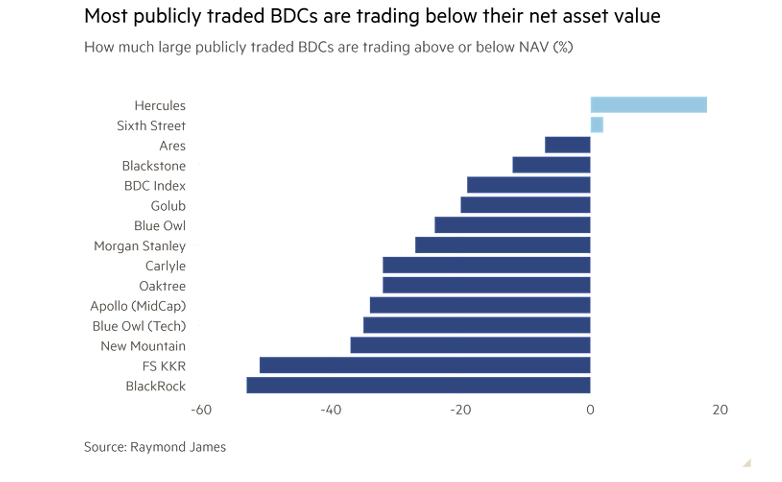

The more fragile part is below the surface with Private credit showing clear signs of strain. Fitch reported that the U.S. private credit default rate rose to 5.7% in January 2026, while many private credit BDCs are now trading below net asset value (NAV), at roughly 82% of their underlying asset value [7]. Concerns may have also centered on the sector’s exposure to software companies, a major borrower group in private credit.

However, the recent sell-off may present a short-term opportunity. This view posits that much of the weakness could be disproportionately driven by fears about AI disruption rather than a broad-based deterioration in fundamentals. Many enterprise software firms are deeply embedded in business infrastructure, with products integrated into core workflows and systems. [8] Their value extends beyond code, encompassing data integration and operational support, which may act as a barrier to replacement even as AI capabilities expand. With recurring revenues and high switching costs, software credit fundamentals may remain relatively resilient, suggesting private credit valuations may recover from current discounted levels if spreads stabilise.

Commodities

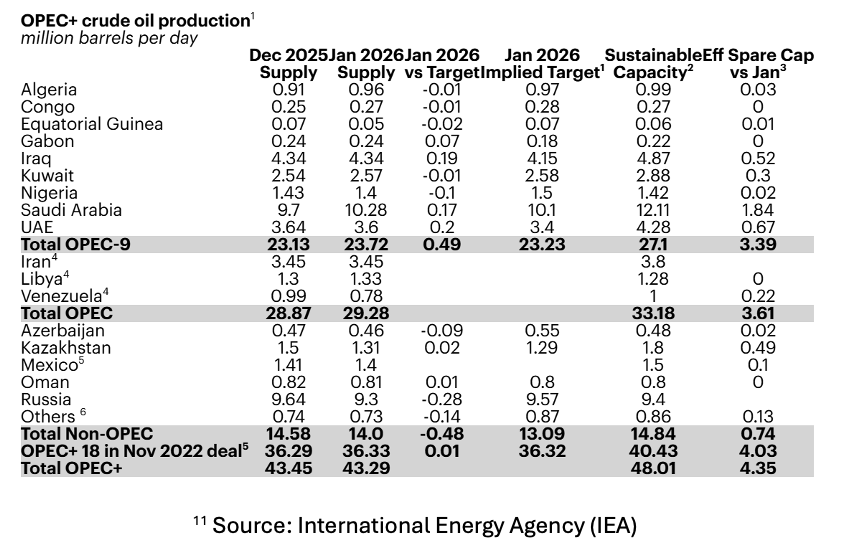

Recent geopolitical tensions involving Iran and several neighbouring oil-producing countries have increased risks to global energy markets. A key concern is the Strait of Hormuz, one of the world’s most important energy chokepoints, through which roughly 20% of global oil consumption and trade flows each day [9]. Escalating tensions have raised safety concerns for tanker traffic, pushing up insurance costs and making shippers more reluctant to transport crude through the region. As a result, tanker traffic has reportedly fallen to around four ships per day compared with a typical average of roughly twenty-four [10].

The disruption currently appears to affect export flows rather than oil production. Producers are still able to pump oil, but security risks and shipping constraints are slowing deliveries to global markets. This distinction is important because flow disruptions often delay shipments rather than permanently reducing supply. Oil can be stored at export terminals or in floating storage and delivered once conditions stabilise, though prolonged disruption could limit the ability of producers to move spare capacity through the region.

Markets reacted to these risks quickly as oil prices rose quickly. However, global oil inventories increased by around 477 million barrels in 2025, providing a buffer that could absorb temporary disruptions. [11]

Overall, the situation will likely keep oil prices higher, particularly if shipping through the Strait of Hormuz becomes further constrained. However, if disruptions remain temporary and deliveries resume, the main effect may be delayed shipments rather than a lasting supply shock. If there is a swift resolution, oil prices in 2026 may still trend downward.

Source :

[1] March Barometer of financial markets outlook | Pictet Asset Management Singapore

[2] Bloomberg Terminal

[3] March Barometer of financial markets outlook | Pictet Asset Management Singapore

[4] The Fed has bought over $90B in Treasury bills since December. Why this has a huge impact on your finances. | MarketWatch

[5] Bloomberg Terminal

[6] The January 2026 Senior Loan Officer Opinion Survey on Bank Lending Practices | US Federal Reserve

[7] Investors ditch private credit funds on rising worries over bad loans | Financial Times

[8] Market Pulse: As AI Disrupts, Not All Software Is Created Equal | iCapital

[9] The Strait of Hormuz is the world’s most important oil transit chokepoint | U.S. Energy Information Administration (EIA)

[10] Global oil and gas prices soar as Iran crisis disrupts shipping, production | CNA

[11] Oil Market Report – February 2026 | IEA