Macro

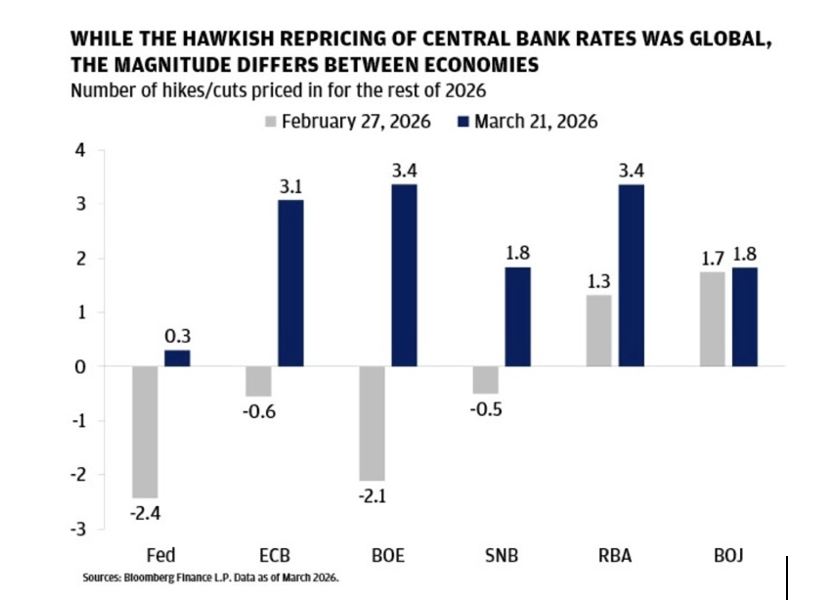

The energy shock from the Iran conflict has triggered a dramatic hawkish repricing of central bank rate expectations globally. As of March 21, markets had moved from pricing 2.4 cuts from the Fed before the war to 0.3 hikes, while the ECB swung from 0.6 cuts to 3.1 hikes and the BOE from 2.1 cuts to 3.4 hikes priced for the rest of 2026 [1]. The repricing has been most severe in Europe, where policymakers are acutely aware of the 2022 experience when the ECB was widely seen as too slow to respond to the energy shock from Russia’s invasion of Ukraine [2]. The ECB has already revised its 2026 headline inflation forecast up to 2.6% from just under 2%, while cutting its GDP growth projection to 0.9% [3].

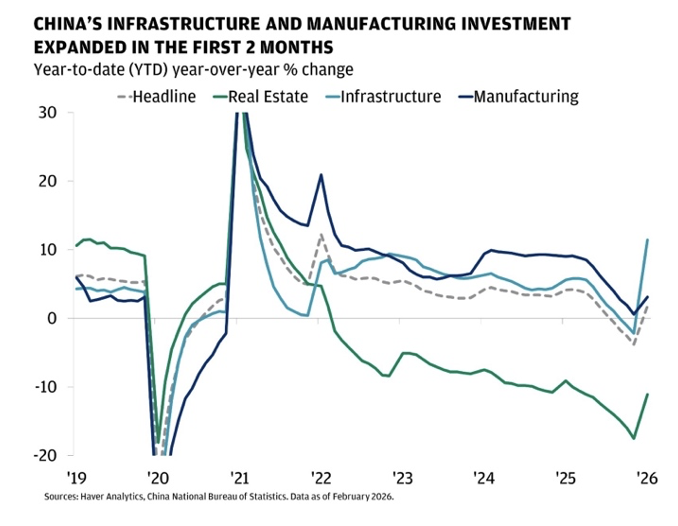

China presents one of the more interesting macro setups heading into the second quarter. Chinese equities may remain a selective opportunity following the March 2026 NPC, where policymakers set a GDP growth target of 4.5 to 5.0% [4] and signalled a continued emphasis on higher-quality, innovation-led growth over broad-based stimulus. Fiscal expenditure, government bond issuance, and central transfers are all set to reach record highs, with total infrastructure and public services investment expected to exceed 7 trillion yuan4. The 15th Five-Year Plan elevates industrial and technological self-reliance as a central strategic policy, with the “AI Plus” initiative, integrated circuits, and advanced manufacturing designated as key growth engines1. Early data supports this tilt: high-tech manufacturing industrial production grew 13.1% year-on-year in the first two months of 2026, contributing 31.5% of overall IP growth [5].

Equities

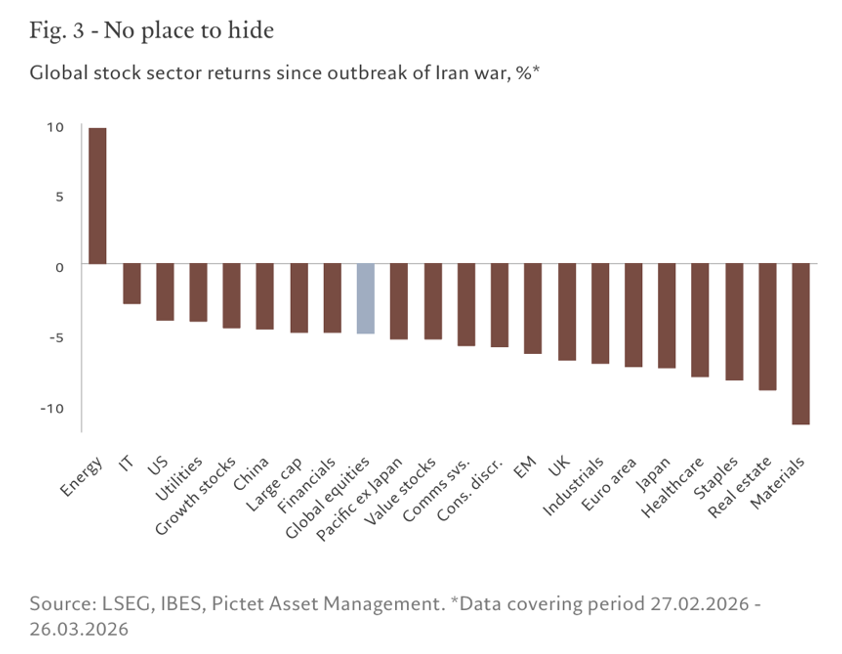

The outbreak of the US-Israeli military campaign against Iran on February 28 has reverberated across global equity markets, with energy the sole sector posting positive returns as Brent crude surged above $100 per barrel on March 27 [6] amid disruptions to shipping. Beyond energy, there has been virtually no place to hide. Materials and real estate have been among the hardest hit, while Asia and Europe appear most exposed given their dependence on Middle Eastern energy imports, with Japan’s Nikkei 225 falling roughly 11% and Europe’s STOXX 600 declining around 6% since the conflict began [7].

Chinese equities, however, appear to stand out as a relative bright spot. China’s large strategic commodity stockpiles, diversified energy supply chains including access to Russian oil, and its accelerating adoption of renewables and electric vehicles give its economy a greater capacity to absorb external shocks than most [8]. Against the backdrop of China’s government policy outlined earlier in the macro section, earnings inflection in strategically aligned sectors, particularly technology, semiconductors, and advanced manufacturing, could be supported. The rapid adoption of AI agents has emerged as a near-term catalyst for large-cap Chinese technology names, reinforcing the policy emphasis on AI as a strategic industry. Offshore Chinese equities have pulled back more sharply than onshore benchmarks in recent weeks, with MSCI China declining approximately 11% from its one-year high compared to roughly 2% for the CSI 300, leaving offshore valuations at a wider discount [9].

Fixed Income

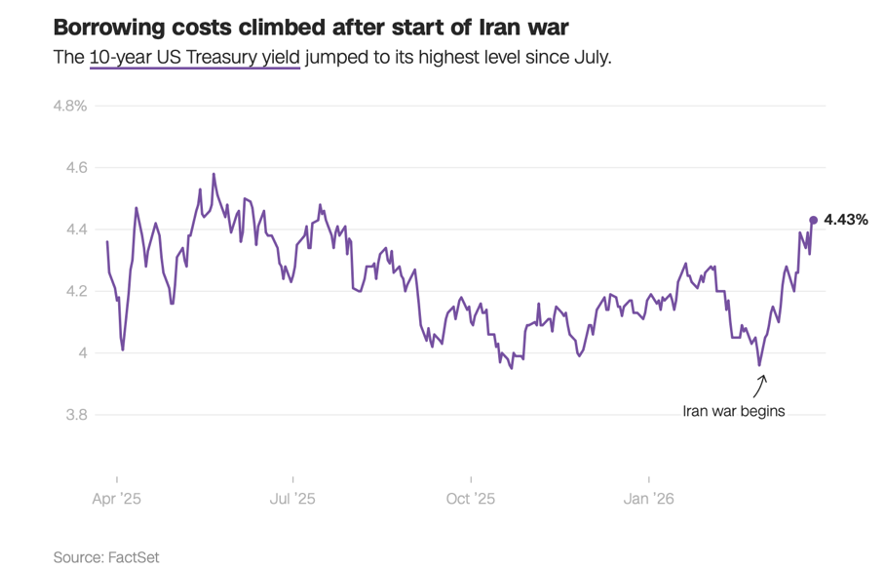

The most striking feature of the current bond market is the breakdown of fixed income’s traditional safe-haven role. Since the outbreak of the Iran conflict, government bonds have sold off alongside equities rather than providing the usual diversification benefit, as the shock is coming through energy prices and inflation rather than a collapse in demand [10]. The US 10-year yield rose alongside the 2-year yields in a classic bear-flattening move as front-end rates reprice the hawkish shift in central bank expectations [11]. Credit spreads have also begun to widen from historically tight levels, with the Morningstar US Corporate Bond Index OAS moving off a low of 0.83 percentage points pre-war [12], though the move so far has been modest relative to the rates repricing.

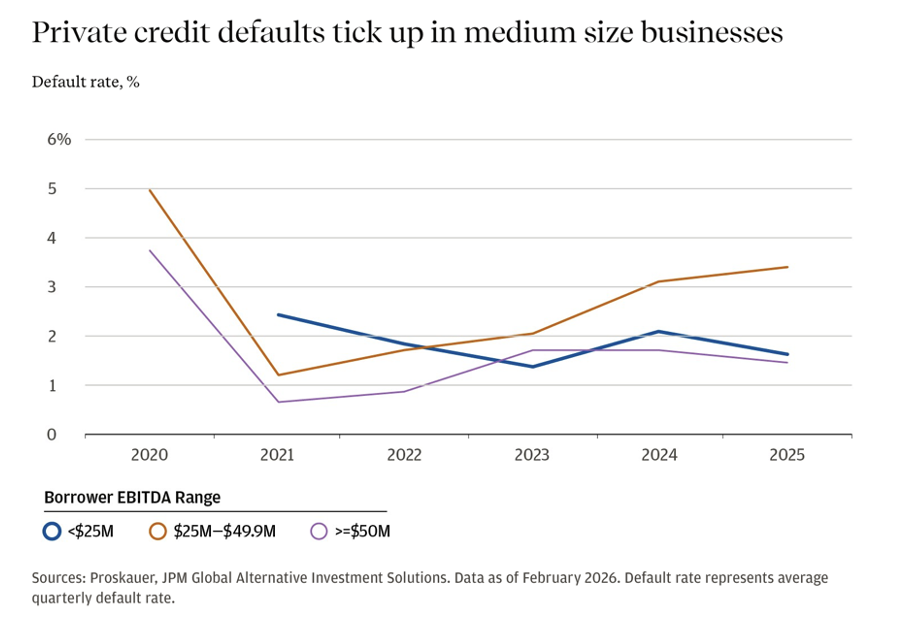

The Iran war has compounded the stress in Private Credit. Several flagship private credit funds have announced withdrawal freezes, exposing the liquidity mismatch inherent in structures offering periodic redemption windows on fundamentally illiquid underlying assets [13]. While private credit’s floating-rate structure and senior secured positioning provide some structural resilience, middle market lending spreads could widen from 500 bps to 650 bps in a downside scenario [14] as energy-intensive borrowers face pressure on coverage ratios.

FX & Commodities

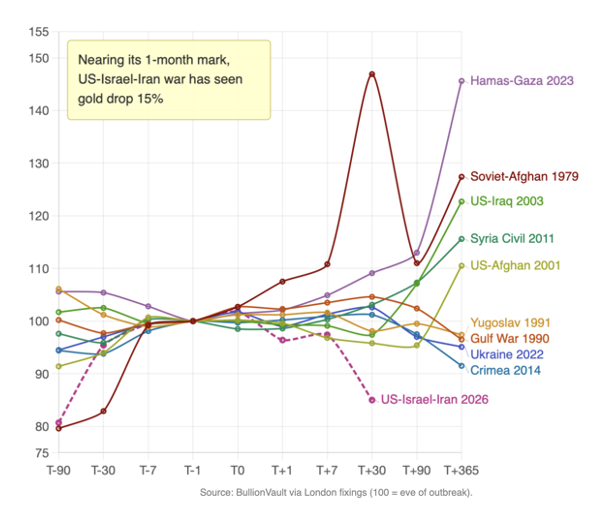

Gold’s sharp decline since the outbreak of the Iran conflict has defied the conventional safe-haven playbook. After briefly spiking above $5,400 in early March, gold has fallen more than 14% since the war began, posting its worst weekly loss since 1983 [15] at one point.

Three factors explain the counterintuitive move. First, surging oil prices have raised inflation expectations and pushed markets to reprice the Fed rate path higher, with traders now seeing less than a 20% probability of a cut over the next year [16] versus more than two cuts priced before the conflict. Higher real yields may increase the opportunity cost of holding a non-yielding asset like gold. Second, haven demand has concentrated in the US dollar rather than bullion, with the dollar index rising nearly 2% since the war began15, which may mechanically pressure dollar-denominated gold. Third, after a 64% rally in 2025, gold positioning was heavily extended, and significant ETF outflows suggest investors have been liquidating appreciated gold holdings [17] to raise cash or cover losses elsewhere in their portfolios. Major banks’ year-end forecasts remain in the $6,000 to $6,300 range [18], suggesting the structural case for gold as a portfolio diversifier with low correlation to equities and bonds over time may remain intact, even as the short-term dynamics have shifted against it.

Source :

[1] China details 2026 policy mix to bolster growth and innovation, share opportunities with world

[2] Iran war fuels central bank rate hike bets on inflation fears | Reuters

[3] European Central Bank holds rates steady, warns outlook is ‘significantly more uncertain’ | CNBC

[4] China details 2026 policy mix to bolster growth and innovation, share opportunities with world

[5] National Economy Got off to a Robust and Promising Start in the First Two Months | China National Bureau of Statistics

[6] Crude Oil Price | Trading Economics

[7] How badly has the Iran war hit the global economy? The tell-tale signs | Al Jazeera

[8] Barometer: Iran conflict demands earnest reassessment of active positions | Pictet Asset Management

[9] China in the Year of the Horse: A stable trot or a brisk gallop? | J.P.Morgan Private Bank

[10] Government bonds are having their safe haven status tested as the Iran war drags on | CNBC

[11] Trump’s Iran War Just Triggered A Second Shockwave — This One Is In The Bond Market | Bezinga

[12] Amid Iran War, Credit Spreads Show Early Signs of Widening | Morningstar

[13] How the Iran Conflict Triggered a Private Credit Liquidity Crisis | The Fulcrum

[14] Conflict in the Middle East: Implications for markets and macro | Allianz

[15] Gold just had its worst week since 1983 | CNN

[16] Gold Heads for Weekly Drop as War in Iran Keeps Oil Prices High | Bloomberg

[17] Why the Gold Price Is Falling During the Iran War—and What it Means | Newsweek

[18] Why gold hasn’t moved since the Iran conflict — and where it could go next | CNBC